Employment report holds the key to where growth is heading

- 03.01.24

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Jobs report holds the key to where growth is heading

- Powell’s testimony to Congress may provide insights

- President Biden needs to talk up his record at the SOTU

Hello March! As we turn the chapter on February and transition into March, there are plenty of exciting events to keep on our radar, from the arrival of spring, to St. Patrick’s Day celebrations, college basketball tournaments and baseball’s opening day. There’s no shortage of fun events to look forward to in the coming weeks! And speaking of major events, there are plenty of big events in the financial markets that are on our radar as well as we head into next week including the February employment report, Fed Chairman Jerome Powell’s semi-annual testimony to Congress and the President’s State of the Union speech. Here are our thoughts on these key events and the ‘state’ of the economy and markets.

- State of the economy | The economy continues to hum along (Atlanta Fed 1Q24 GDP estimate: +3.0%), albeit shifting down a notch from the pace seen in the final quarters of last year. Consumption has remained remarkably resilient thanks to persistently low unemployment and solid income growth. However, some cracks are starting to appear (e.g., soft retail sales report, rising delinquency rates, particularly on credit cards, and falling savings). And with employment growth continuing to prop up the consumer, the health of the jobs market holds the key to where economic growth goes in 2024. No doubt January’s hotter than expected employment report (+353k) and stronger inflation print (core CPI: +0.4% MoM) showed the economy was on firmer footing than policymakers expected heading into the new year. That’s why we and policymakers will be tuned into next week’s employment report, which should show some payback from January’s blockbuster job gains (Consensus +200k, RJ +180k).

- State of the Fed | Chair Powell’s delivers his semiannual Monetary Policy Report to both chambers of Congress next week. All eyes will be watching Powell’s testimony for any insights on the timing and pace of the Fed’s upcoming easing cycle. The market’s optimism for excessive rate cuts at the start of the year has been unwound given the latest batch of stronger than expected economic data. Case in point: the market was expecting an ~80% chance of a 25 bps rate cut in March at the beginning of the year, but this has been removed as the market now expects the Fed’s initial cut to be delayed until June. This is more in line with the Fed and our economists' view for where rates are heading over the remainder of the year. While Powell is not likely to declare victory, the mood on Capitol Hill should be brighter than the last time he met with Congressional leaders (June 2023) given that banking sector woes have subsided, the economy and jobs market remained resilient and disinflationary trends continued. While Powell is likely to be pressed about the direction of the monetary policy, he will stick to his script, urging patience on the rate cutting front as policymakers wait for more data to confirm that inflation is falling sustainably toward their 2.0% target.

- State of the election | Next week, President Biden will host his State of theUnion address. This will be a particularly important speech for the president, as he currently has the lowest approval rating of any president (39%) at this juncture in his presidency and is trailing former President Trump in the polls (most notably in all six major swing states). As the economy remains the key issue for voters, we expect President Biden to highlight his achievements in this area, particularly as there seems to be a strong disconnect between voters’ perception and the actual strength of the economy. While household net worth is at all-time highs, the S&P 500 is up 11% on an annualized basis since the start of Biden’s presidency, and the U.S. has had the strongest recovery of any G7 country, only 23% of voters believe that his policies have helped them. That compares to the 50% that believe that Trump’s policies did. Even worse, over 50% of voters still believe that the economy is currently in either a recession or depression. With only a few levers at the Administration’s disposal (e.g., spending in the CHIPS and IRA, potential tax cut bill), we expect the president to outline his reelection campaign themes and policies to attempt to keep the economy on solid footing.

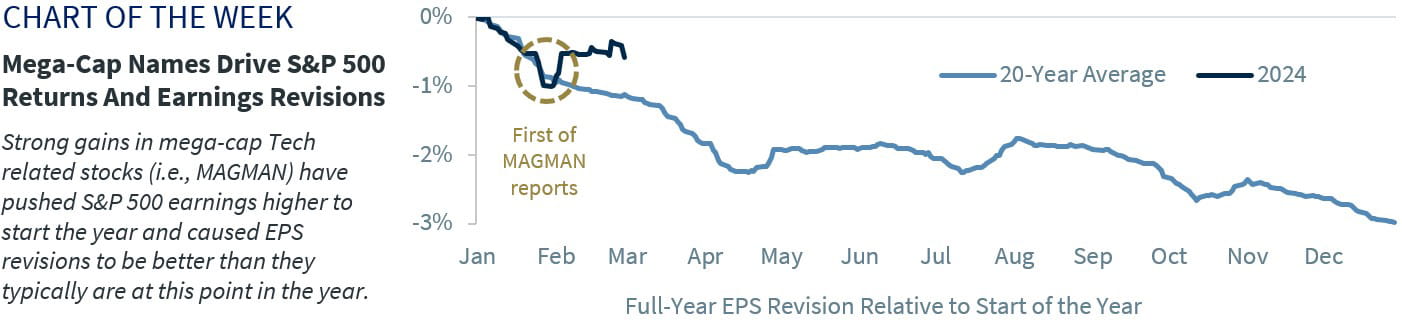

- State of earnings | With over 99% of the S&P 500 market cap having reported up until this point, the 4Q23 earnings season is essentially complete. The S&P 500 posted its second consecutive quarter of EPS growth (+5% YoY, a slight deceleration from the +7% pace in 3Q23), but there was significant dispersion beneath the surface. Earnings in the fourth quarter were driven by the Tech-related names, as a composite of MAGMAN (MSFT, AAPL, GOOGL, META, AMZN, NVDA – which makes up ~20% EPS weight of the S&P 500) saw their earnings rise ~68% YoY, while the rest of the Index saw their earnings decline 6%. Overall, these trends are expected to continue throughout 2024 and have been reflected in the revisions year-to-date. MAGMAN expects to see their earnings increase ~25% in 2024, while the rest is expected to see a more modest 8%. MAGMAN has also seen their 2024 earnings estimate revised 6% higher since the start of the year, while the rest of the Index has been revised 2% lower.* The strength of the mega-cap Tech names has helped to support earnings revisions overall, as 2024 S&P 500 earnings have been downwardly revised only 0.3% since the start of the year. Typically, earnings have been revised ~4x lower at this juncture over the last 20 years.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.